Hsmb Advisory Llc Fundamentals Explained

Hsmb Advisory Llc Fundamentals Explained

Blog Article

The 6-Minute Rule for Hsmb Advisory Llc

Table of ContentsAll About Hsmb Advisory LlcNot known Details About Hsmb Advisory Llc The Basic Principles Of Hsmb Advisory Llc Excitement About Hsmb Advisory LlcHsmb Advisory Llc for BeginnersThe Facts About Hsmb Advisory Llc RevealedLittle Known Questions About Hsmb Advisory Llc.

Be mindful that some plans can be pricey, and having specific wellness problems when you apply can boost the premiums you're asked to pay. You will need to ensure that you can afford the costs as you will certainly require to commit to making these payments if you desire your life cover to continue to be in placeIf you really feel life insurance can be beneficial for you, our partnership with LifeSearch permits you to get a quote from a variety of suppliers in double fast time. There are different types of life insurance coverage that aim to fulfill various security needs, consisting of degree term, reducing term and joint life cover.

Excitement About Hsmb Advisory Llc

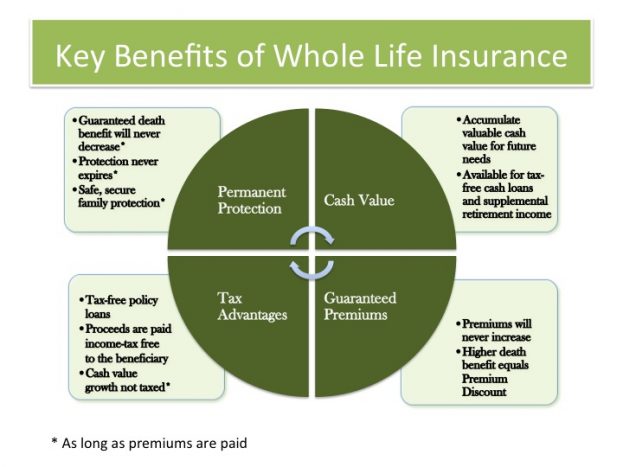

Life insurance policy offers 5 economic advantages for you and your family (Insurance Advise). The major advantage of including life insurance policy to your economic plan is that if you die, your successors receive a swelling sum, tax-free payout from the plan. They can utilize this money to pay your final costs and to change your income

Some policies pay out if you create a chronic/terminal disease and some offer financial savings you can use to sustain your retirement. In this article, find out regarding the various benefits of life insurance coverage and why it might be a good concept to buy it. Life insurance coverage uses advantages while you're still to life and when you die.

Not known Factual Statements About Hsmb Advisory Llc

If you have a policy (or policies) of that dimension, the individuals who rely on your revenue will certainly still have money to cover their ongoing living expenditures. Beneficiaries can use plan benefits to cover important everyday expenditures like rental fee or home mortgage settlements, energy costs, and groceries. Typical annual expenses for homes in 2022 were $72,967, according to the Bureau of Labor Data.

Getting The Hsmb Advisory Llc To Work

Development is not affected by market problems, permitting the funds to build up at a stable rate with time. Furthermore, the cash worth of entire life insurance policy grows tax-deferred. This means there are no earnings tax obligations accumulated on the cash value (or its growth) up until it is taken out. As the cash money worth accumulates over time, you can use it to cover costs, such as acquiring a cars and truck or making a down repayment on a home.

If you determine to borrow against your money worth, the loan is exempt to earnings tax obligation as long as the plan is not surrendered. The insurer, nevertheless, will certainly bill interest on the lending quantity until you pay it back (https://nowewyrazy.uw.edu.pl/profil/hsmbadvisory). Insurance provider have differing rates of interest on these car loans

Getting The Hsmb Advisory Llc To Work

For instance, 8 out of 10 Millennials overestimated the price of life insurance policy in a 2022 research study. In truth, the typical price is closer to $200 a year. If you think buying life insurance policy may be a smart monetary step for you and your household, take into consideration seeking advice from a financial expert to embrace it into your monetary strategy.

The five main types of life insurance are term life, whole life, universal life, variable life, and last expenditure coverage, likewise understood as funeral insurance policy. Whole life starts out setting you back extra, however can last your whole life if you keep paying the premiums.

How Hsmb Advisory Llc can Save You Time, Stress, and Money.

Life insurance policy can likewise cover your home mortgage and provide cash for your family to keep paying their costs (https://www.indiegogo.com/individuals/37505142). If you have family depending on your revenue, you likely need life insurance to support them after you pass away.

Generally, there are two sorts of life insurance policy plans - either term or long-term plans or some mix of both. Life insurance providers supply various forms of term plans and typical life plans along with "rate of interest sensitive" products which have come to you could try this out be much more widespread considering that the 1980's.

Term insurance offers defense for a specific time period. This period can be as brief as one year or provide protection for a particular variety of years such as 5, 10, two decades or to a specified age such as 80 or in many cases as much as the oldest age in the life insurance coverage mortality tables.

The Basic Principles Of Hsmb Advisory Llc

Presently term insurance rates are extremely competitive and among the least expensive traditionally seasoned. It should be kept in mind that it is an extensively held belief that term insurance coverage is the least expensive pure life insurance policy protection offered. One needs to review the plan terms carefully to make a decision which term life alternatives appropriate to satisfy your specific scenarios.

With each new term the costs is raised. The right to restore the plan without proof of insurability is an important benefit to you. Or else, the danger you take is that your health and wellness might deteriorate and you may be not able to get a policy at the very same rates and even at all, leaving you and your beneficiaries without coverage.

Report this page